Performance Benchmarks

In rigorous Optuna-tuned cross-validation studies, Murphet consistently outperforms Prophet for bounded metrics.

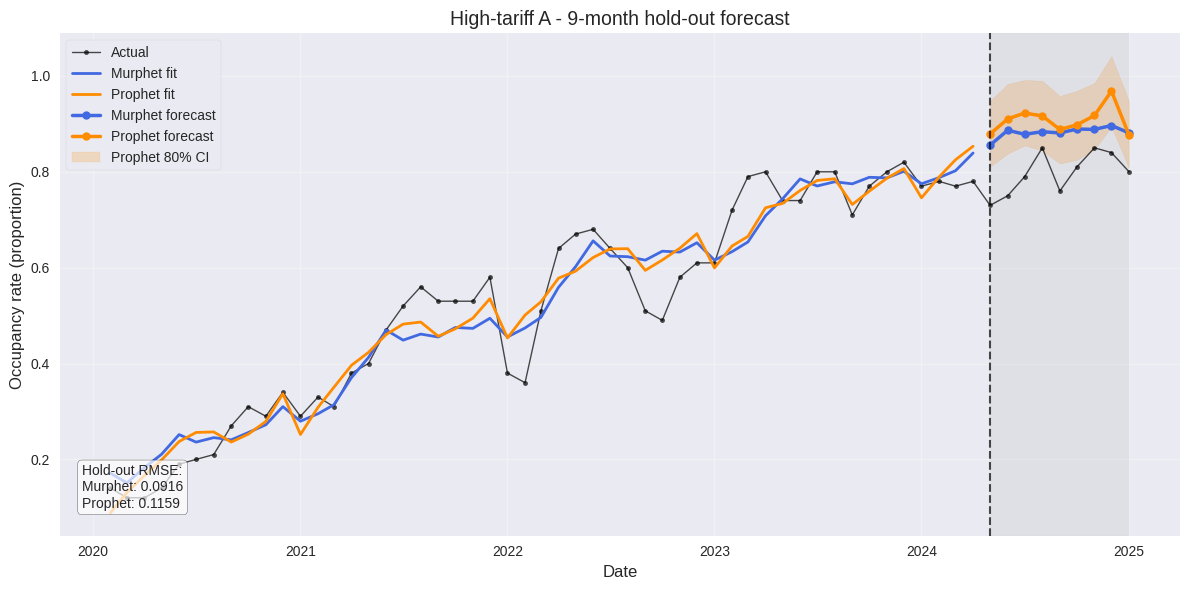

Hotel Occupancy (High Tariff A)

9-month hold-out test:

Murphet RMSE: 0.091 | Prophet RMSE: 0.158

42% error reduction

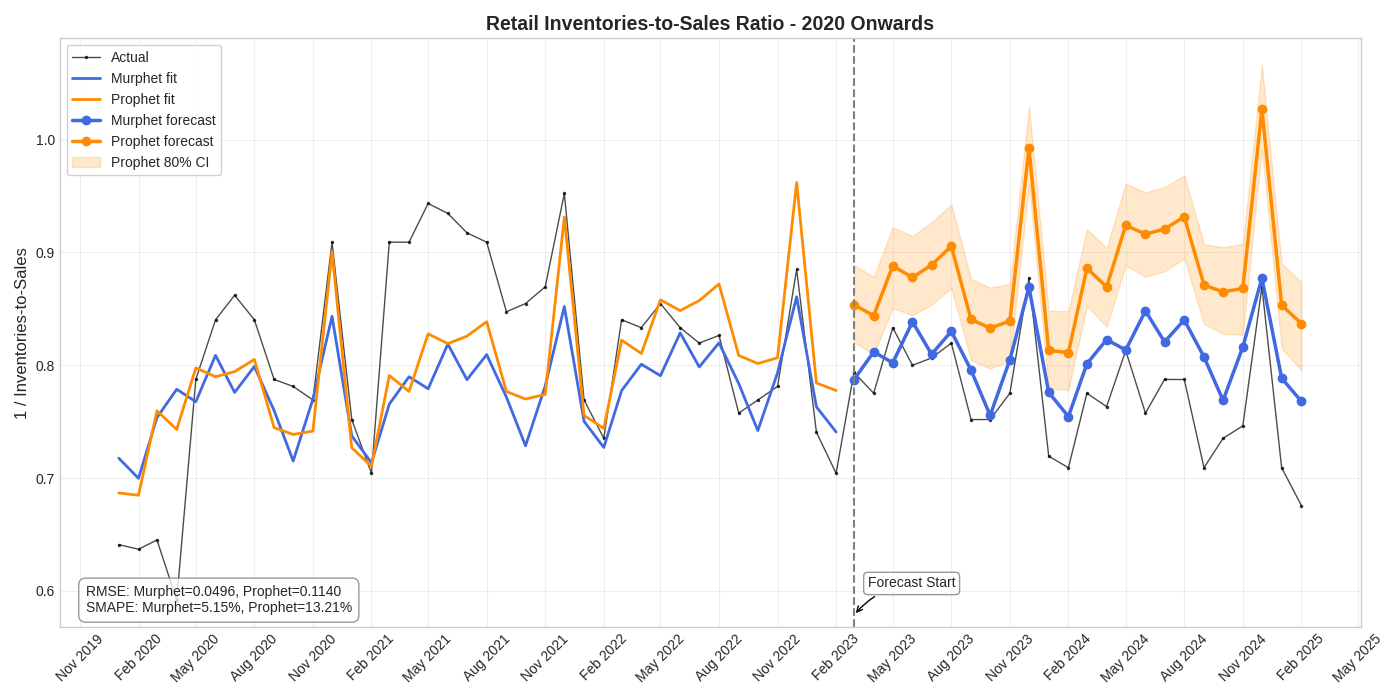

Retail Inventories-to-Sales Ratio

12-month hold-out test:

Murphet RMSE: 0.050 | Prophet RMSE: 0.114

56% error reduction

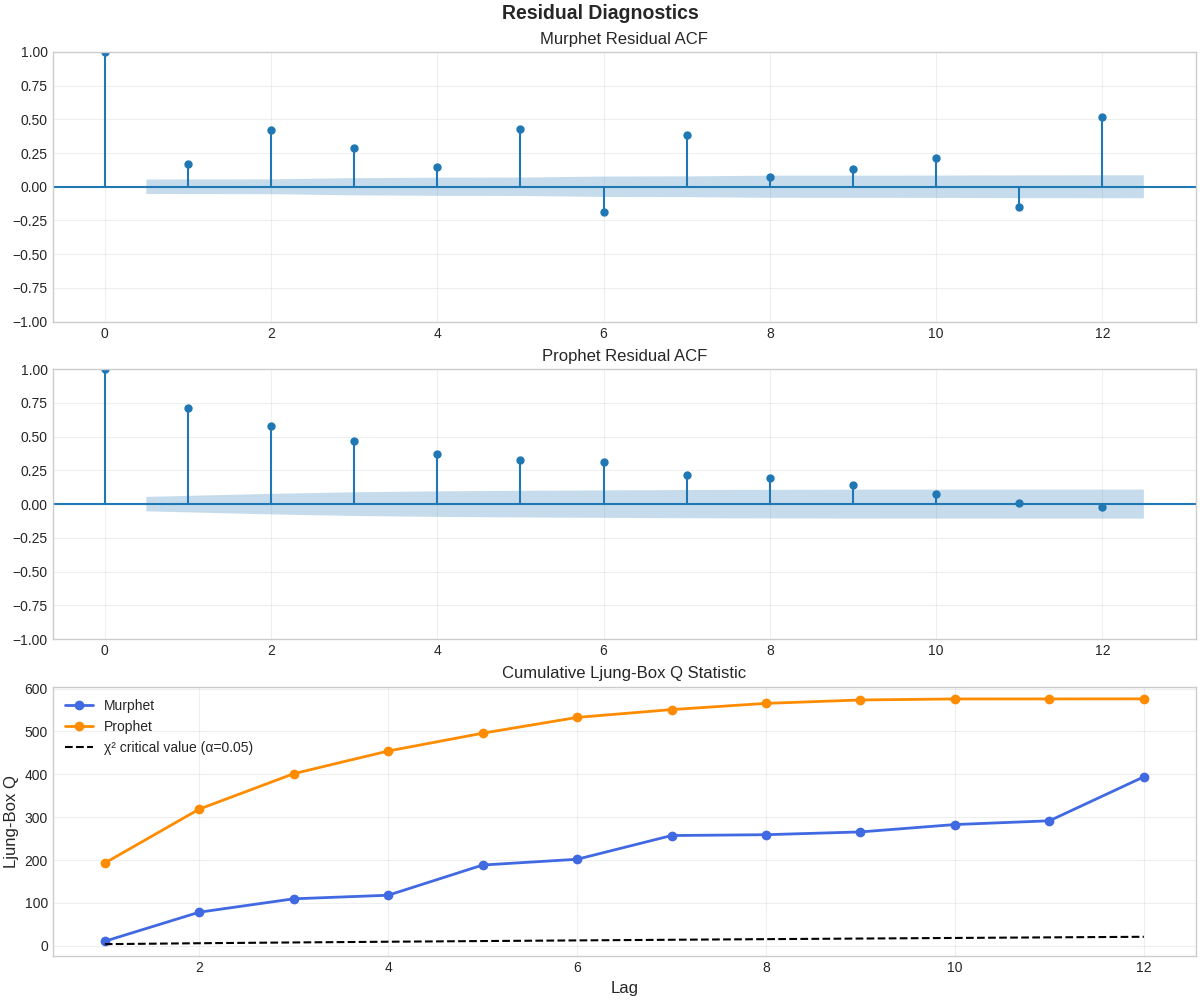

Residual Analysis

Murphet's residuals show significantly lower autocorrelation and reduced Ljung-Box Q statistics, indicating better capture of underlying patterns and more reliable predictions.

Migrating from Prophet to Murphet

If you're already using Prophet for forecasting rates or proportions, transitioning to Murphet is straightforward:

# --- Prophet code ---

from prophet import Prophet

m = Prophet(

changepoint_prior_scale=0.05,

seasonality_prior_scale=10.0,

seasonality_mode='additive',

mcmc_samples=0

)

m.fit(df)

future = m.make_future_dataframe(periods=12)

forecast = m.predict(future)

# --- Equivalent Murphet code ---

from murphet import fit_churn_model

model = fit_churn_model(

t=df['t'], # Numeric index

y=df['y'], # Target values (between 0-1)

likelihood="beta", # For bounded metrics

delta_scale=0.05, # Same as changepoint_prior_scale

season_scale=1.0, # Similar to seasonality_prior_scale/10

periods=12.0, # Yearly seasonality

num_harmonics=3, # Complexity of seasonal pattern

inference="map" # Fast point estimates (like mcmc_samples=0)

)

future_t = np.arange(df['t'].iloc[-1] + 1, df['t'].iloc[-1] + 13)

forecast = model.predict(future_t)